One of the most common methods of payment in both traditional and online retail is payment by credit or debit cards. This is particularly true since the pandemic started as more and more shoppers are looking to avoid touching cash and prefer to pay with contactless payment options. After all, card-based payments are reliable and trustworthy ways to accept payments easily. But there are a lot of things to consider when choosing a new payment processor. Here’s what retailers should consider to minimize their costs when signing up with a new card processor:

Type of Payment Options

The type of retail business you have determines the way in which you take payment. There are 3 general types of payment options:

Card Terminals (EMV PIN Pads) for merchants to accept in-person payments

Virtual Terminals for merchants to manually accept payments with the card payer present (e.g. phone or fax payments)

Payment Gateways for customers to make payments themselves in the shopping cart of an online store (e.g. PayPal, Bambora, Stripe, etc.)

Each of these types of payments can be supplied by the same or differing payment processors but they each have different rates. Generally speaking, card terminals have the lowest rates and are considered the most secure because the card holder must be present and / or provide verification with a PIN code. Remember that magnetic stripe readers are not EMV compliant and only chip-and-PIN terminals protect the merchant against chargebacks.

Expert Tip: While card terminals are EMV compliant and do protect merchants against chargebacks, this is usually only for in-person payments made using chip-and-PIN. Since the pandemic started, more and more retailers are offering contactless (tap) payments. But if you do accept contactless payment as a merchant, you should always check your payment processing policy to see if tap payments have chargeback liability. Many processors do not cover tap payments and so merchants may be on the hook for any chargebacks on such payments. This is why many merchants have a tap limit and it is definitely something a merchant should check if they’re thinking of increasing their tap limit.

Virtual terminals have higher card rates than card terminals but they are still generally lower than payment gateways. Merchants should keep in mind that virtual terminals still open the merchant to chargeback liability. The best way for retailers to minimize the liability exposure is to make sure that there is a customer-signed order agreement and for the merchant to collect as much verification information as possible such as billing address, etc.

Finally, there are payment gateways. This is the payment option for e-commerce which generally has the highest fees as it’s considered the highest risk of the 3 options. Similar to virtual terminals, online payments are liable to chargebacks. Merchants selling online should always check with their gateway payment provider for their chargeback policies and how they can best protect themselves from them.

Types of Payment Processing Fees

Even when you know what payment options work for a retail business, various processors will have offer different types of processing fees:

Flat % Fee + ¢ per transaction

Interchange Plus % + monthly fees

CAD vs. Foreign Currency

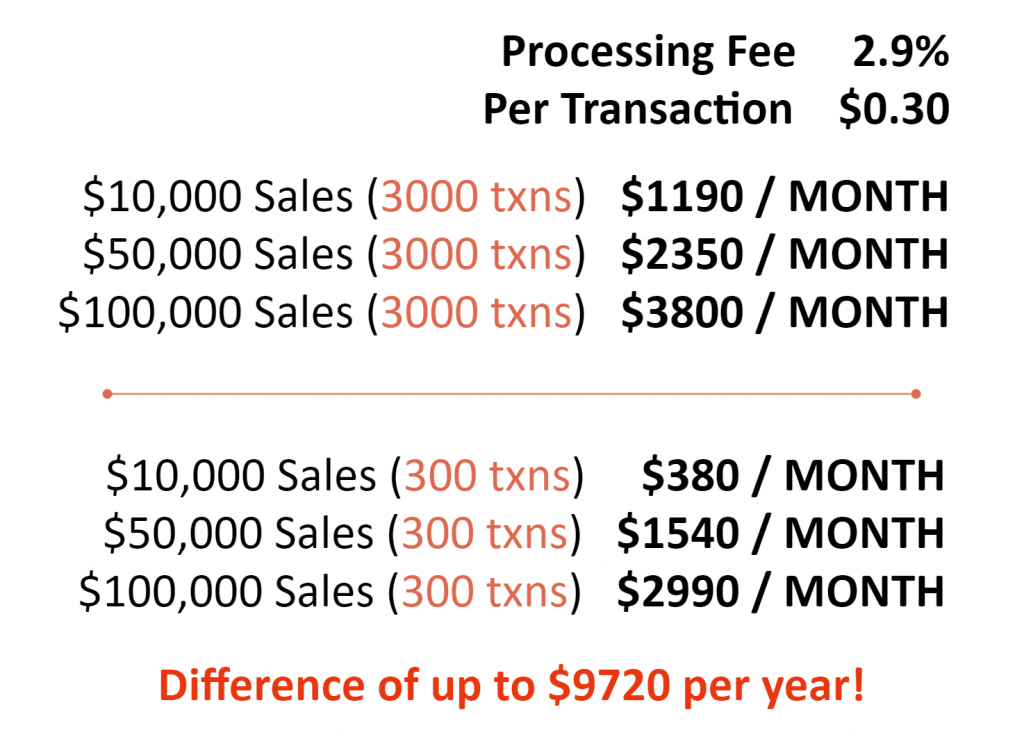

Credit card processing fees often range between 1.55%-4% with variable rates from Mastercard, Visa, Discover and American Express. Some credit card processors charge more for particular credits cards (eg. American Express) because American Express relies more heavily on merchant swipe fees and annual fees rather than interest rates (that most other processors make money on).

Everything else being equal, merchants should compare different processing fees based on three factors:

The average number of transactions per month

The average dollar value of every transaction

The total value of all sales processed per month

Here’s an example of how processing fees can be dramatically different based on variations in the 3 factors above. Merchants should always compare the rates between processors before signing a new processing agreement.

Expert Tip: While Interchange Plus rates often work best for retailers with fairly high processing volume (e.g. $1M+ annually), it’s important to consider the type of clientele a merchant has. This is because Interchange Plus processing fees charge different rates based on the type of cards used (e.g. gold cards cost merchants more than standard credit cards). As such retailers who sell luxury or high-end products may be better off with a flat % monthly fee if the majority of their clients are customers with premium or foreign currency cards.

POS Payment Integration

Traditionally, merchant processing is handled separately for in-store and online payments. While this is changing now with a few all-in-one payment solutions coming out, besides the overall cost of the processing fees, the biggest cost to managing retail payments is the amount of resources required to track payments against sales.

After all, reconciling payments received is key to making sure that all funds are received and to quickly find out when there are any operational issues that need to be addressed immediately (e.g. suspicious employee behavior, high refunds, etc.)

This is why more and more retailers are looking for POS that can handle their preferred payment processor whether for online or in-store payments. Having payments automatically recorded in the POS minimizes human error and increases checkout speed which is important for stores with higher traffic.

Individual merchants will value different features but, generally speaking, the more established the retailer, the more important it is for the merchant to minimize sales-based fees that take a percentage of sales. While some software solutions have low (or even no) monthly costs, it’s usually because they charge higher than average % fees and / or restrict you from choosing other payment options by charging additional transaction fees on top of the regular payment fees. Others like TAKU Retail charge a flat monthly software fee with no additional sales-based % fees.

Other things to look out for in a retail POS is whether it allows refunds in-store regardless of where a payment is received. Many systems were designed to accept sales separately from different sales channels. As such, it can be a hassle to manage returns and accept refunds in separate systems. Systems like TAKU Retail allow merchants to manage even online returns with store-based refunds or exchanges. This allows merchants to not only encourage exchanges instead of refunds to avoid losing the entire sale, but it allows merchants to refund with lower cost payments options such as cash or debit as many payment processors charge the same rate for refunds as for sales.

Other Things to Consider

Retailers also need to be wary of other a few other factors when choosing their credit card processors to ensure that they are well-protected and aware of the real cost:

The amount of time required (withholding period) for funds to be deposited into the company bank account.

Whether processing fees are deducted upfront (Net Deposits) or at the end of every month (Gross Deposits) – net deposits can be harder for bank reconciliations as the original sales amounts won’t be on monthly statements.

Whether payment processing statements are all-in-one or separate for different sales channels.

Whether there are additional monthly fees and minimums.

Want to read more articles? You can find our latest article on retail shrinkage here

It’s no secret that retail is no longer a one-step shopping experience. Customers want the flexibility of taking their in-store experience online and vice versa. In 2020, Walmart responded to the global pandemic by improving their omnichannel experience and adding more square footage to their stores for online order fulfillment. This helped them achieve a 97% spike in e-commerce sales.

A study by First Insight showed that customers in many categories still prefer in-store shopping versus buying online. In particular, the study showed that over 70% of shoppers are more likely to make impulse purchases or buy more in store, because of the merchandising and customer experience.

It’s just that the pandemic has made it more likely that the customer journey starts online, even if the actual purchase happens in a physical store. As such, for traditional merchants, it’s not about whether customers are shopping more online or in-store. It’s about needing to serve customers across multiple channels, often at the same time. This is why the entire omnichannel shopping experience is increasingly important.

But if you’re a traditional retailer just starting out in this brave, new world, where do you start? Changing store processes to serve omnichannel shoppers isn’t something that can happen overnight. This is where “clicks-to-bricks” strategies come in.

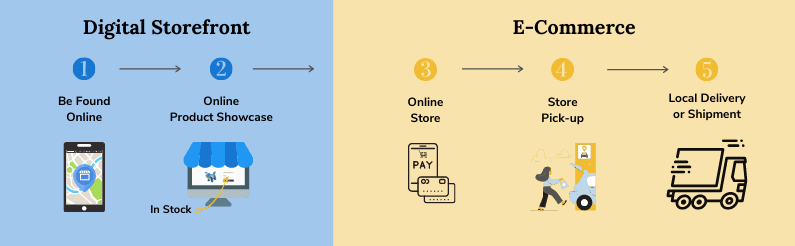

Clicks-to-bricks simply refers to strategies that focus on using “digital storefronts” or “pre-shopping discovery” online to drive foot traffic into stores instead of encouraging customers to mainly shop online. Even if you offer delivery, there are a lot of benefits to focusing on store-driven online shopping.

Top 5 Advantages of a Clicks-to-Bricks Strategy

It maximizes local awareness of your business online. During the pandemic, a lot of businesses focused on selling online and neglected the fact that store shoppers also start their buying journey online. Whether it’s checking store hours or stock availability, being found online is key to offering a smooth customer experience. The easier it is for shoppers to find you online, the more likely they are to purchase from you as compared to some of your competitors who may not be as easy to find.

It increases sales per shopper. Shoppers buy more when shopping in store. Retailers want customers to buy in store because they are more likely to make additional impulse buys with higher margins. If store products are linked to online search with tools such as Google’s See What’s In Store (SWIS) or Local Inventory Ads (LIA), you’ll get store shoppers that walk in “ready to buy” as they already know what you carry and have on your shelves. In fact, helping customers “pre-shop” or “discover” products online can drive more traffic to both physical and online stores. This will increase overall sales per shopper as you’re able to serve shoppers in multiple channels.

It maximizes profitability. Besides bigger basket sizes, using online awareness to drive higher quality foot traffic to your store means that you’ll be spending less in marketing for higher sales. If you use omnichannel tools that link your store data with online research, you can even save on the cost of having employees or agencies manage your product information online.

It gives you useful customer insights. Connecting with customers on multiple channels means more opportunities to gather information about your customers. Whether it is an email address or a physical address, having more data increases retailers’ insights into their customers and their buying habits, making marketing easier and cheaper over time.

It gives you useful inventory insights. Knowing what sells well on which channel allows retailers to sell and target specific segments when releasing new products or product lines.

Multi-location retailers have more issues managing multiple stores because no one can be at more than one place at a time. In order to run a multi-location business, even when you are not always there, you should look at processes that have an impact on productivity and customer satisfaction. We have put together a list of things to help retailers manage their multi-location retail businesses, so that their business can run smoothly no matter where they are.

Multi-location means that you will have different people working in stores that may not interact with each other on a day-to-day basis. Managing each store effectively means standardizing and automating processes so that they all run with the same efficiency. These processes can range from onboarding new employees, delivering product knowledge, processing returns, to updating inventory.

While it’s not easy finding the resources and time to document processes, having something written down will significant speed up future training and make it much easier for staff to understand your policies and procedures. The most successful retailers are those who can a provide consistent experience to customers across all locations. After all, the experience a customer has in a store is a significant part of the brand image of a retailer.

2. Use cloud technology to centralize and streamline your business processes

Cloud technology helps sync up and organize inventory, customer history, employee performance, sales, and cashflow. This means that you can manage your entire business from a single system. Having a centralized location for all business data allows retailers to get accurate, real-time feedback into how their business is running and identify any gaps in their workflows.

One of the best parts about using cloud technology is that it gives you mobile accessibility. You’re no longer tied to a single computer and can have access to your business data on-the-go to see changes in your store as they happen. While some solutions will give you access to your sales data from anywhere, a lot of the modern, new cloud retail management systems will let you access and manage all of your business data so that you can run your store from anywhere.

Another benefit to using cloud technology is that it automatically helps you backup your business data in the cloud. Unlike older store systems which require manual backups or expose you to hardware failure, even if you lose power during a storm, all of your business information will be safely stored in the cloud. And as long as you have smartphones, you can continue to sell using mobile devices.

3. Improve retail business inventory control

It is crucial to have accurate inventory and stock data at all times. One of the major problems with running a multi-location business is that it is much harder to keep your product information in sync. This has only gotten worse since the pandemic started since more retailers are also selling online. The best retail companies are those that use technology that gives them visibility into their inventory and stock levels at every point of storage. Having products available exactly when customers want to buy them is best in an ideal world but helping customers (e.g. shipping to their home or directing them to another location) even when a product is not in stock is key to customer service and closing every sale.

Other ways to control your inventory include keeping an eye on your re-stocking schedule (which requires knowledge of lead times and seasonal availability) as well as your minimum stock levels. This is so that stores are able to re-fill stock before selling out.

4. Use a single commerce system

To make sure that store data and reports are all in-sync, retailers need a single, smart commerce system that can handle both store sales and online orders. Combining your POS and e-commerce processes into a single system helps you determine what products should be carried, which items are bestsellers across different locations or online sales channels, and which products need to be discounted or discontinued across your entire business. Using a single system also helps employees deliver the same experience to customers wherever they shop.

5. Secure your data

In order to comply with local and national privacy laws, retailers need to do their best to protect the privacy of both customers and employees. Finding the right software and hardware to manage sensitive information is key to building customer trust and keeping retail businesses healthy.

TAKU Retail stores customers data on separate databases to minimize the risk of privacy breaches. Read more about our security features here.

Want to know more about our multi-location capabilities? Read more.

The bottom line is, you want to make a profit with your business. This means selling products and services that customers want and are willing to pay for at the price you are selling. Finding that point can be confusing to many business owners: balancing margins and finding out the going market price are things to consider before releasing a new product. The wrong strategy could lead to large financial losses; we have created a pricing guide to help retailers get to the other side and find the right pricing strategy for your business.

Cost-based pricing

This is the most straightforward way to determine sell prices. This method is not related to market pricing and sets prices based only on actual costs. In this case, retailers estimate all fixed (e.g. purchase cost) and a share of variable costs (e.g. overhead costs that you have to pay even without any sales such as rent, payroll or utilities) to determine the sell price of a product. This method is most commonly used in product categories that are highly competitive where market prices are relatively known. Staple products or commodities are common examples.

Cost-plus pricing

Instead of adding the actual overhead cost of the business, cost-plus pricing is a lot easier to calculate as it assumes a specific fixed markup percentage to a product’s purchase cost. For example, some merchants will simply multiply the cost to buy a product by a factor of 2x to 3x. This is called the price markup. While this method is much easier to use, it is important for retailers to make sure that the markup percentage is enough to meet your target rate of return (profit) and to periodically review the markup to make sure that it is still suitable.

Value or market-based pricing

This is the most common method in industries where the perceived value of a product is highly driven by emotion or lack of availability such as fashion, art, luxury cars or concessions at sporting events. Essentially, this method sets prices mainly based on the perceived or estimated value of a product or service to the customer rather than according to the cost of the product or historical prices. This is commonly used by retailers with deep understanding of brand building, market pricing, managing exclusivity and valuing the benefit to a customer versus how much she or he is willing to pay.

While market-based pricing is constantly changing, and therefore more sophisticated to manage, with newer technology, it is increasingly possible for retailers to incorporate value-based pricing into their pricing strategy to avoid “leaving money on the table.” It’s also worth pointing out that the increasing number of merchants going online has also made pricing in some categories more transparent which increases price competition and can drive pricing lower. It’s why many premium brands enforce MSRP on their online retailers (e.g. Apple) and more merchants are selling their own branded products online today as these categories are the most likely to be successful since supply can be more easily controlled and substitutes are less available.

Penetration pricing

Introducing new products into the market by lowering price is a strategy that some retailers use to introduce their products into a saturated market. This is a good chance to build brand loyalty and to get new customers to try your products.

Although it may seem intuitive to jump into the market with this strategy to gather as many customers as possible, this strategy does have some drawbacks. Raising prices (after the initial release) often leads to some reluctance from customers, so proceed with caution.

Sensitivity to price changes

All of the pricing methods above should not be applied without considering whether a product is price elastic or inelastic. Price elasticity refers to how sensitive price changes will have on the demand for a product. For some products, demand will change significantly if prices are changed and vice versa. A classic example is grocery store bread. Unless brand loyalty is strong or there is a special product feature, bread pricing tends to be elastic: as price increases, the demand will decline.

Price elasticity is useful as it gives you a sense of how much you can adjust pricing without significantly affecting the demand for your product. It’s important to remember that many products have category thresholds. This means that even if you sell an product that is price inelastic or not sensitive to price changes (e.g. luxury purses), the market will have a perception of the maximum a buyer is willing to pay.

Similarly, it is important to remember that demand sensitivity is also impacted by the availability of substitutes or competitors. So if you sell in a category that has a lot of competitors with similar alternative products, the demand for your products will most likely be more sensitive to price changes since it’s easier for your buyers to find replacements.

Want to read more on how to manage inventory effectively?

Inventory control helps retailers determine what products are selling well versus the ones that are not. Having stock control helps retailers make the most profit with their inventory. This gives retailers an indication on how much more or less stock they need. This, in turn, helps reduce operational and storage expenses.

This is especially important for brick-and-mortar retailers because controlling the amount of stock they have on hand is directly related to customer satisfaction and how much profit they make on their inventory. Understanding how to manage this is vital to a retailer’s success since inventory is the largest resource and use of cashflow for every merchant.

TAKU Retail client, Kam Wai Dim Sum, raves about TAKU’s reporting functions. Thanks to TAKU, they are now able to use their POS system to track their daily sales and know which are their best performing items. Read more here.

Maintaining a minimum stock level means stores have to keep a minimum number of products in stock to make sure they are always able to replenish their shelves easily. This is especially so with retailers during busy and uncertain seasons: this could mean extended delivery delays or stockouts. Instead of guessing or approximating, retailers need to calculate the ratio of delivery times to stock levels so that they are optimizing their inventory and lowering their operational costs.

Keeping tabs of stock levels and maintaining a healthy and lean stock level means that retailers are able allocate resources to new products to satisfy new customer wants and needs. Having a higher turnover is a positive sign for retailers because it means that they are able to sell more and make more sales.

Tips for Better Retail Inventory Control:

Using real-time retail POS software that tracks inventory movement across all channels based on actual stock levels

Using a barcode scanner to accurately track products as they are sold or received

Running inventory counts to make sure that stock levels in the POS match the quantities actually on the shelves

Tracking the sale of inventory items to know which products are bestsellers and which items don’t need to be re-stocked

By always having some stock on hand and determining your ideal reorder days, retailers do not ever have to worry about running out of certain items and long lead times. Knowing what stores have in-stock may seem straightforward with a single store location. But it is a lot more difficult for multi-location retailers to track inventory across different locations and manage returns and exchanges easily. This is especially true as retailers today often sell the products both in-store and online. TAKU Retail’s inventory management capabilities mean that retailers are able to automatically see real-time inventory levels at all times, regardless of how many locations or online sales channels they are selling in.

Learn more about TAKU Retail’s inventory management capabilities.

👇👇👇 Scroll to Download our COVID-19 Survival Tips for Retailers!!

There’s no denying that we now live in a physically and digitally connected world. The benefits of being globally interconnected are visible in the growth and stability of the world economy over the past decade since the 2008 global financial crisis. But history and economies are cyclical. We were already looking at a potential downturn before the recent coronavirus global pandemic started but retailers are now looking at the most unpredictable global business environment in decades. This is where retail crisis management helps to give businesses options to manage the unknown.

For businesses that were launched in good times, owners will now need to quickly adapt to the challenges of managing uncertainty and risk. Like any other business, owning a retail store comes with its fair share of risks. Even at the best of times, store owners must deal with operational risks that impact cash flow. After all, the US economy was strong for the majority of 2019, yet U.S. retailers still lost 50.6 billion due to inventory shrinkage alone.

With the help of new technology, there are ever more ways to tackle theft and organized retail crime, but they are not the only challenges facing retailers today. Whether it’s a natural disaster in the form of a fire or flood, supply chain disruptions, or an employee ranting about the company on social media, unexpected retail risks can have a huge impact on your bottom line.

Fortunately, there are some things you can do to help minimize the risk of unexpected emergencies, plan for interruptions to your retail business, and do your best to protect your employees, assets, and reputation.

I’m not by any means a risk management expert. I am, however, a repeat small business owner. So I know what it’s like to face the terror of a sudden downturn AND not be prepared to deal with negative cash flow. If any of the tips below help others minimize their stress or better prepare for the next crisis, that’s good enough.

External Threats

Environmental disasters are external crises that are generally out of the control of any one private business. These include forest fires, hurricanes and, of course, global health pandemics. Because these are environmental and often cannot be predicted, these are often the most costly. They usually impact the economies of entire countries, can cost billions of dollars in damage to affected businesses and homes, and require a long recovery time. Besides the $1 billion in lost sales experienced by retailers during hurricanes Katrina and Harvey, these disasters resulted in $125 billion in property damage.

Business Insurance for Major Disasters

Nobody really likes to purchase business insurance but it’s often critical to the survival of a company in the face of a business-interrupting disaster. Even if you don’t live in an area that is prone to serious storms or other seasonal events, you need to make sure you have enough insurance to cover fire/water damage for your inventory, assets or property. Not only is this type of coverage mandatory on some leaseholds, it’s the only way to protect yourself against legal claims if there is 3rd party damage during an incident, which is also a key part of retail crisis management.

It’s important to remember that environmental disasters can be considered “acts of God” or “force majeure” and can nullify some insurance depending on your carrier and the type of plan you have. While some companies will step up at times of crises, you shouldn’t count on the possibility of coverage in the middle of a disaster if your plan has such exemptions. This is exactly why you should always read your insurance policy to understand what type of financial coverage you are actually buying. If the language in the fine print is too much, write to your insurance broker to make sure they give you a clear written response on what coverage you get with your insurance premiums

Technology, Flexibility and Adaptability

Adaptability for a business today is often tied to flexibility and technology. How flexible your processes are will determine how quickly you can adapt to different market environments. For retailers, this means using technology and tools that will allow you to immediately change how you are selling or taking payment with customers. The latest cloud systems not only automatically back-up your data, they work on any device and allow you to sell wherever your customer is. So when your store suddenly loses power, you can switch from your till to your mobile phone to keep selling.

For retailers dealing with the impact of COVID-19, for example, shutting down may not be an immediate option. Small businesses who cannot afford to shutdown or are looking for better ways to manage the impact are encouraged to:Download our free checklist

Add or Expand Digital Sales Channels including e-commerce for shipment or pick-up in store.

Offer Contactless “Leave At My Door” Delivery with prepaid orders online, by phone, fax or email.

Make sure you have a Google My Businessprofile and keep your store hours up-to-date.

Encourage Visible Hygiene Management in store by having all staff use gloves or wear masks. Have hand sanitizers readily available at the checkout area, near doors with handles, etc.

Encourage Social Distance In Store by increasing the space in the checkout area between cashiers and where shoppers are waiting to pay. Stop offering samples unless they are pre-packaged.

Encourage “Contactless” Payments (e.g. tap or Apple Pay) and discourage the use of cash to protect your staff wherever possible. You may want to increase your “contactless” limit with your merchant processor but remember that you are liable for any potential chargebacks on “contactless” payments.

Minimize Any Processes that Require Touch such as loyalty programs that require a tablet. Print out a QR code or signage for your web site and encourage users to sign up on their own phones.

Sell In Store Gift Cards with an Incentive (e.g. extra $15 for every $100 gift card) to encourage shoppers to come back to the store when things are back to normal.

Offer Free Pens to shoppers who don’t have their own. It’s a cost-effective gift that discourages the use of public pens and helps customers remember you. Remember to minimize touch when offering them.

Communicate Proper Treatment Procedures when staff are sick. Make sure all managers and staff know what to do when they are sick. There is a lot of information out there – be sure to refer to the most credible medical sources in your country. In Canada, that will mean the public health authorities for your province or territory. In the US, the CDC is a reliable authority for guidance. For further details, you can also review the steps to prepare worksplaces for COVID-19 published by the WHO.

Limit Stock Quantities for any essential household and medical products to avoid stock outs.

Internal Threats

Not all emergencies are external. There are a number of internal risks within a company, many of which aren’t any less significant to the survival of a business than, for example, a natural disaster. You’ll want to work with workplace safety experts if your workplace involves food, hazardous materials or any type of production but for most of us in retail, cash flow, reputation and operations crises are usually top-of-mind for small business owners.

Cash Flow is the Lifeblood of a Business

I’m not the first business owner to say that timing is everything when running a business. During good times, this can refer to being in the right place when unusual opportunities present themselves. During bad times, this refers to whether you are financially in a position to survive when there is an interruption to the business. And more often than not, retail crisis management refers to your cash flow position because you need to have access to liquidity or credit to be able to get through an unusually slow period – you can’t sell hard assets quickly or for a good price in the middle of a crisis. So yes, while a natural disaster is completely unexpected and is out of anybody’s control, what you can control is the position you are in when disaster strikes.

I’m certainly not trying to preach about the virtues of keeping unused cash in the bank (assuming there is even any) instead of reinvesting in the business, etc. But if you haven’t already, you may want to get approved for a line of credit only for emergencies when the business is booming or you have the opportunity to. The key is to get credit when you don’t need it and to not use these emergency resources for any daily operations. Yes, hindsight is 50-50, and this won’t help you if you’re already dealing with an emergency but history does repeat itself so can better prepare yourself for the future.

Operations Resilience Planning

Operations covers many different parts of a business. It’s not possible to list every area a business owner or manager can review but, by and large, most retailers should always have some sort of plan in place for:

Succession or delegation if management is incapacitated

Data loss or privacy breaches

Supply chain breakdown

1) Management Incapacitation

Nobody ever wants to think about a scenario in which they aren’t around. But the fact is, if you are a small business owner, you are likely an employer and others depend on you for their livelihood. You can plan for every possible risk but if you cannot issue payroll, approve payments or make important decisions when they need to be made, you’re exposing your business to extra risk. Make sure you have a contingency plan in place for your own responsibilities including who is authorized to access company bank accounts during an emergency. Speak to your accountant or lawyer to learn more about the options.

2) Data Loss or Privacy Breaches

Just as many people rely on smartphones to remember all of their contacts, the data you use to run and track your business is irreplaceable. In a retail business, this usually refers to your POS data. Not only is the information stored in your POS system critical to your business decisions (e.g. how much product to order based on sales, etc.), it’s also a legal requirement in most countries to both collect sales taxes and report profitability.

Not only do natural disasters damage physical structures like storefronts and warehouses, they can also lead to a loss of important company files and data. Environmental disasters aside, as a business, you are also exposed to ransomware or database hacks on a daily basis. Luckily data security is definitely something you can more affordably control now in the age of cloud computing. It doesn’t matter what type of technology you use in your business operations. Don’t take a chance with unexpected damages or hardware failure with your business data. Store it in the cloud, or better yet, use a cloud POS system so that you can run your business from anywhere. After all, even if your data is secure, you need access to your POS system and other retail management tools to be able to continue operating.

With GDPR in Europe and ever more privacy regulations everywhere around the world, it’s important for small businesses to start on the process of developing and implementing a privacy strategy to protect their reputation with customers. There’s no point stressing out over the fact that you may have missed certain regulatory deadlines. Regulators and customers everywhere would rather see that a company has a plan and is working on improving rather than giving up or saying “it doesn’t apply to me.” For some basic steps you can take to get started on how to better manage privacy in your small business, you can refer to this blog post.

3) Supply Chain Breakdown

If just one link in a retailer’s supply chain is broken, it can have a significant impact on business operations and profit. Which is why retailers need to be able to react quickly to unexpected supply chain events – whether it is a natural disaster, supplier failure, political or labour strife.

While there is no way to prevent these events from taking place, there are measures you can take internally to minimize the impact of such disruptions and be better prepared including:

Retail Crisis Management is Risk Management

Having total supply chain visibility involves looking at possible environmental, social, and political risks. Identify possible “what-if” scenarios – what happens if a supplier is facing a weather disruption and loses power? Do you have an alternative source? What if there are transportation delays? What if political events drive up prices of raw materials? These “what-if” scenarios are numerous and may seem unlikely to occur in the first place. But it’s important to know what that list looks like first so that you can start to develop contingency plans to have more options when an unexpected crisis does take place.

Look at manufacturing and distribution coverage

Depending on the size of your business, broaden your connections by reaching out to suppliers in different networks and regions. Seeking out alternate suppliers in different locations will help you re-route orders if one of your suppliers is negatively impacted by an external event.

Transport flexibility

Unexpected issues and events can arise when inventory is being transported to and from distribution centers. For instance, merchandise can be stolen, delays can occur, and weather disruptions can cause damage to roads and transport routes. To prepare for these risks, it’s important to have transport flexibility. In other words, if one avenue of delivery is disrupted, ensure that you have the capability to switch and depend on another logistics channel. If instead, you opt to go for a third-party logistic provider, it’s a good idea to ensure that they can also provide the same kind of flexibility.

Remember that changes in lead times with suppliers during a major disaster will likely change the speed and cost of transport you will need. Do a cost analysis of what your business can afford to spend to get products to you and make sure you have the credit or cash flow necessary to fund the upgrades. During an emergency, you may need to consider foregoing profits or even taking a loss simply to keep enough revenue flowing through the business to cover fixed overhead costs.

Reputation Management

Brand reputation and reputation management are critical to a retailer’s success. In fact, a report done by Total Retail shows that 90% of shoppers have chosen not to purchase from a company because of its bad reputation. Which is why consumers are increasingly relying on reviews to determine the quality of a business.

But, certain circumstances can arise that can quickly impact the viability and perception of your brand – e.g. a distraught employee publicly telling off a customer, poor management of health risks, etc. – creating distrust amongst consumers, and so on.

Help your retail business build a reputable brand and better prepare for compromising situations:

1) Be transparent about company policies and preventative procedures

In the case of an external crisis, consumers start distrusting businesses. Under these circumstances, it’s best to get ahead of the situation by reassuring employees, suppliers, partners and shoppers that you are taking preventative action or being as proactive as you can. During the recent coronavirus pandemic, StichFix made sure that members were aware of the rigorous cleaning process their clothing goes through between rentals to minimize any fears customers had about the cleanliness of renting clothes.

2) Manage negative reviews promptly

Gathering customer reviews is one of the best ways to make a good impression on a potential shopper. And even if you receive negative feedback, remember that it’s normal (and more realistic) for companies to receive a few bad reviews, just as long as you respond promptly and clearly show to customers that you are taking action. To learn more about customer review management and how to respond to reviews, click here.

3) Clearly communicate staff expectations

Setting clear company expectations with every new employee will pay off in the future when you’re trying to contain a potential public relations emergency. You may not be comfortable with the unconventional employee handbook Telsa gives its employees but the point is that you can’t expect employees to know what you expect without giving them some guidelines. Depending on the size of your business, it shouldn’t be an extensive document but it’s worth those late nights or legal fees to get one prepared since you will be sharing it repeatedly in your company. And, of course, communication doesn’t stop with orientation or handbooks. Part of retail crisis management is clearly communicating with employees and setting a good example during and after any crisis. There’s no better way for senior management to walk the talk.